All Categories

Featured

Table of Contents

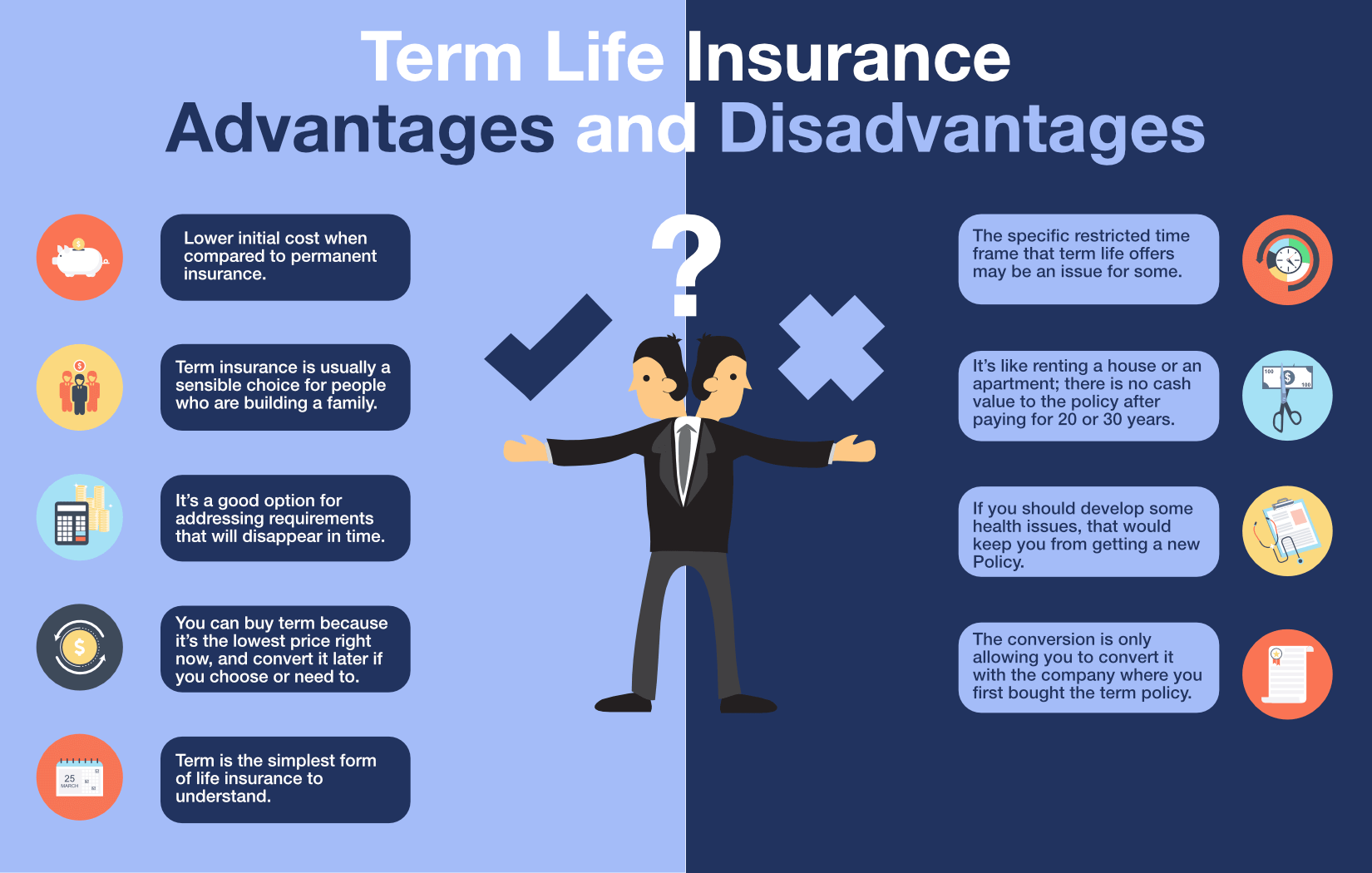

There is no payment if the policy runs out prior to your death or you live beyond the policy term. You may be able to restore a term policy at expiration, yet the costs will certainly be recalculated based on your age at the time of renewal.

At age 50, the premium would certainly increase to $67 a month. Term Life Insurance Policy Rates three decades old $18 $15 40 years old $28 $23 50 years old $67 $51 Resource: Quotacy. Quotes are for a $250,000 30-year term life plan, for males and ladies in exceptional health. On the other hand, below's a take a look at rates for a $100,000 whole life plan (which is a sort of irreversible plan, meaning it lasts your life time and consists of money worth).

The Term Illustration In A Life Insurance Policy Refers To

Rate of interest rates, the financials of the insurance company, and state regulations can likewise influence premiums. When you think about the amount of coverage you can obtain for your premium dollars, term life insurance coverage has a tendency to be the least expensive life insurance policy.

He purchases a 10-year, $500,000 term life insurance plan with a costs of $50 per month. If George dies within the 10-year term, the policy will certainly pay George's beneficiary $500,000.

If George is diagnosed with an incurable ailment during the initial plan term, he probably will not be qualified to restore the plan when it runs out. Some plans offer ensured re-insurability (without proof of insurability), however such functions come at a greater cost. There are several sorts of term life insurance policy.

Normally, most companies provide terms varying from 10 to three decades, although a couple of offer 35- and 40-year terms. Level-premium insurance (term life insurance vs ad&d) has a set regular monthly settlement for the life of the plan. Many term life insurance policy has a degree costs, and it's the type we've been describing in most of this write-up.

A Whole Life Policy Option Where Extended Term Insurance Is Selected Is Called An

Term life insurance policy is eye-catching to youngsters with kids. Parents can obtain significant coverage for a low cost, and if the insured passes away while the plan holds, the household can rely upon the survivor benefit to replace lost earnings. These policies are also well-suited for people with expanding households.

The right choice for you will depend upon your demands. Below are some points to consider. Term life policies are perfect for individuals that desire significant insurance coverage at an affordable. Individuals who have entire life insurance policy pay much more in costs for much less insurance coverage but have the safety and security of knowing they are safeguarded forever.

The conversion cyclist should enable you to transform to any kind of irreversible policy the insurance provider uses without restrictions - which of the following life insurance policies combined term. The main features of the cyclist are preserving the initial health rating of the term policy upon conversion (also if you later have wellness concerns or become uninsurable) and making a decision when and just how much of the insurance coverage to convert

Certainly, general costs will increase dramatically because whole life insurance is much more costly than term life insurance. The advantage is the guaranteed authorization without a medical examination. Medical conditions that develop throughout the term life duration can not trigger premiums to be boosted. Nonetheless, the business may call for restricted or full underwriting if you intend to include extra motorcyclists to the new policy, such as a long-term care cyclist.

Term life insurance policy is a reasonably economical way to supply a round figure to your dependents if something takes place to you. It can be a great option if you are young and healthy and balanced and support a family members. Whole life insurance coverage features considerably higher regular monthly premiums. It is implied to supply insurance coverage for as lengthy as you live.

What Is A Term Life Insurance Rider

It depends on their age. Insurance policy firms established a maximum age restriction for term life insurance policy policies. This is typically 80 to 90 years of ages yet may be greater or lower depending on the company. The costs also rises with age, so an individual aged 60 or 70 will pay substantially greater than a person years more youthful.

Term life is somewhat similar to auto insurance coverage. It's statistically not likely that you'll require it, and the costs are money down the tubes if you do not. If the worst occurs, your household will receive the benefits.

This plan style is for the customer that requires life insurance coverage yet want to have the ability to choose just how their cash value is spent. Variable plans are underwritten by National Life and dispersed by Equity Providers, Inc., Registered Broker/Dealer Associate of National Life Insurance Policy Company, One National Life Drive, Montpelier, Vermont 05604.

For J.D. Power 2024 honor details, go to Long-term life insurance policy creates cash money worth that can be borrowed. Plan loans accumulate passion and unsettled plan fundings and passion will certainly decrease the death benefit and cash worth of the policy. The amount of cash money worth readily available will normally depend upon the kind of permanent policy purchased, the quantity of coverage bought, the length of time the plan has actually been in force and any kind of outstanding plan loans.

What To Do When Term Life Insurance Expires

A total statement of coverage is discovered just in the plan. Insurance coverage policies and/or associated cyclists and features might not be readily available in all states, and policy terms and problems might vary by state.

The major distinctions between the different kinds of term life plans on the marketplace have to do with the length of the term and the coverage quantity they offer.Level term life insurance policy includes both degree costs and a level survivor benefit, which means they stay the very same throughout the duration of the policy.

, also known as an incremental term life insurance coverage strategy, is a plan that comes with a fatality advantage that raises over time. Common life insurance coverage term sizes Term life insurance is budget friendly.

Although 50 %of non-life insurance owners mention cost as a reason they don't have coverage, term life is just one of the most inexpensive type of life insurance coverage. You can frequently get the insurance coverage you require at a manageable rate. Term life is easy to handle and understand. It provides protection when you most require it. Term life uses financial defense

during the duration of your life when you have major monetary commitments to fulfill, like paying a mortgage or moneying your youngsters's education and learning. Term life insurance policy has an expiration day. At the end of the term, you'll need to buy a brand-new plan, renew it at a greater premium, or convert it right into irreversible life insurance policy if you still want coverage. Rates might differ by insurance company, term, coverage quantity, health and wellness course, and state. Not all policies are available in all states. Price illustration valid as of 10/01/2024. What factors impact the price of term life insurance policy? Your prices are identified by your age, sex, and health, along with the insurance coverage amount and term length you choose. Term life is a good fit if you're looking for a budget friendly life insurance policy policy that just lasts for a collection amount of time. If you need irreversible insurance coverage or are thinking about life insurance policy as an investment alternative, entire life may be a far better choice for you. The major differences between term life and entire life are: The length of your insurance coverage: Term life lasts for a set duration of time and afterwards runs out. Typical month-to-month entire life insurance policy rate is determined for non-smokers in a Preferred wellness classification, acquiring a whole life insurance coverage plan compensated at age 100 used by Policygenius from MassMutual. Prices might differ by insurance firm, term, coverage amount, health and wellness course, and state. Not all policies are offered in all states. Temporary life insurance policy's temporary plan term can be an excellent option for a few scenarios: You're awaiting authorization on a long-lasting plan. Your plan has a waitingduration. You're in between tasks. You wish to cover short-lived responsibilities, such as a lending. You're improving your health or way of life(such as quitting smoking)before obtaining a conventional life insurance plan. Aflac supplies many long-lasting life insurance policy policies, including whole life insurance, final cost insurance policy, and term life insurance. Begin chatting with an agent today to read more concerning Aflac's life insurance coverage items and locate the right alternative for you. One of the most preferred type is now 20-year term. The majority of companies will not offer term insurance to a candidate for a term that ends past his or her 80th birthday . If a plan is"renewable," that means it proceeds active for an additional term or terms, approximately a defined age, even if the wellness of the insured (or other variables )would create him or her to be turned down if he or she requested a new life insurance policy policy. Costs for 5-year eco-friendly term can be level for 5 years, then to a new rate mirroring the brand-new age of the insured, and so on every 5 years. Some longer term policies will certainly assure that the premium will certainly notincrease during the term; others do not make that assurance, enabling the insurance coverage firm to increase the rate throughout the policy's term. This indicates that the plan's owner has the right to alter it into a long-term kind of life insurance policy without extra proof of insurability. In the majority of sorts of term insurance coverage, consisting of home owners and car insurance, if you haven't had a case under the plan by the time it ends, you get no reimbursement of the premium. Some term life insurance policy customers have been miserable at this outcome, so some insurers have created term life with a"return of costs" function. The costs for the insurance coverage with this feature are usually significantly higher than for plans without it, and they usually call for that you keep the policy active to its term or else you surrender the return of premium benefit. Weding with young youngsters-Life insurance policy can aid your partner keep your home, existing way of life and give for your children's assistance. Single moms and dad and sole income producer- Life insurance policy can help a caretaker cover child care expenses and various other living costs and satisfy prepare for your child's future education and learning. Weding without youngsters- Life insurance policy can provide the cash to satisfy economic responsibilities and assist your spouse hold onto the properties and lifestyle you have actually both strove to accomplish. However you may have the choice to convert your term policy to long-term life insurance coverage. Insurance coverage that secures somebody for a defined period and pays a survivor benefit if the covered person passes away during that time. Like all life insurance policy policies, term insurance coverage helps preserve a family members's monetary wellness in situation an enjoyed one passes away. What makes term insurance coverage different, is that the guaranteed individual is covered for a detailsamount of time. Since these policies do not give long-lasting coverage, they can be fairly budget-friendly when compared to an irreversible life insurance policy plan with the exact same amount of coverage. While most term plans supply reputable, short-term security, some are more flexible than others. At New York Life, our term policies provide a special combination of features that can aid if you come to be handicapped,2 come to be terminally ill,3 or merely want to transform to an irreversible life plan.4 Because term life insurance offers short-lived security, many individuals like to match the length of their policy with a vital turning point, such as repaying a home loan or seeing kids via college. Level costs term can be extra reliable if you desire the costs you pay to continue to be the very same for 10, 15, or twenty years. Once that period ends, the amount you spend for protection will increase yearly. While both types of coverage can be reliable, the choice to select one over the various other boils down to your specific needs. Since no one recognizes what the future has in store, it is very important to ensure your protection is dependable sufficient to satisfy today's needsand versatileadequate to assist you prepare for tomorrow's. Here are some crucial aspects to remember: When it pertains to something this crucial, you'll desire to see to it the firm you make use of is economically audio and has a tested background of keeping its promises. Ask if there are features and advantages you can make use of in instance your needs change later on.

{kind=link}

Latest Posts

Funeral Insurance For Over 80

Mortuary Insurance

Free Burial Insurance For Seniors